Statement regarding DC governance

This is the Trustee’s statement regarding DC Governance as required under regulation 23 of the Occupational Pension Schemes (Scheme Administration) Regulations 1996, as amended (the ‘Regulations’).

The Scheme is primarily a defined benefit scheme, but holds a number of money purchase benefits. This statement sets out how the Scheme has met the governance standards required by legislation in respect of those money purchase benefits during the Scheme year ended 31 March 2020.

The money purchase benefits held in the Scheme arise from the historic payment of AVC contributions and the transfer of money purchase benefits from the Corah Pension and Life Assurance Plan. The money purchase benefits are held in 17 different investment arrangements. No further money purchase contributions are being paid to the Scheme. The Scheme is not being used as a qualifying scheme for automatic enrolment purposes.

The Trustee publishes this statement to the Scheme’s website annually to ensure it is accessible to members.

Default arrangement

The Scheme has no default (investment) arrangements for the purposes of the Regulations and so the aspects of the Regulations applying to default arrangements are not dealt with in this statement.

Processing financial transactions

The Trustee has a duty to ensure that core financial transactions (including the transfer of member assets into and out of the Scheme, switches between investments and payments to and in respect of members) relating to the money purchase benefits are processed promptly and accurately.

Such transactions are undertaken on the Trustee’s behalf by the Scheme’s administrators: the Coats Pensions Office (CPO) and XPS. The Trustee has agreed service levels (SLs) with the administrators which cover all administration tasks including the accuracy and timeliness of the processing of financial transactions. The existing service levels were reviewed by the Trustee in June 2018 after the Scheme was set up and the Trustee is satisfied that they are within the market norms.

A key element of accuracy in processing financial transactions is data quality, and the Trustee reviewed the work carried out by the predecessor schemes to assess whether any additional work was required to improve the data quality of the Scheme. As a result of that review the Trustee commissioned a review of scheme-specific data from the administrators and has an action plan in place of tasks to improve that data, which is part of their ongoing commitment to review and improve data quality where possible.

The key processes the administrators have in place to ensure that the SLs are met are;

• a task-logging system which is reviewed weekly for forthcoming workloads, with tasks allocated daily;

• daily review of bank balances;

• weekly reconciliation of bank balances;

• protocols to ensure each payment goes through an agreed multi-level review and sign off process (which varies by amount and administrator).

The Trustee’s Audit, Risk and Administration Committee (ARAC) review the administrators’ internal controls on behalf of the Board and the SLs and agreements in place. The administrators prepare quarterly administration reports which are reviewed by the ARAC, which include performance against SLs, highlight any issues or failure to meet the agreed service levels and provide reasons for and details of the resolution of any SL breaches (if applicable).

At the end of the period under review, due to the impact of COVID-19, the Trustee agreed an extension to service levels and carried out a review of the Trustee’s transfer value calculation methodology, suspending the issue of transfer value quotations from 2 April 2020 whilst that review was carried out. Members were kept informed of any delay in providing them with details of their benefit and transfer values were reinstated on 27 April 2020. The ARAC continues to monitor the quarterly reports provided by Administrators to check ongoing compliance against the agreed service levels.

The ARAC further monitored core financial transactions during the year by considering member feedback (if any) including complaints.

Based on the above, the Trustee is satisfied that over the year covered by this statement:

• the Administrators were operating appropriate procedures, checks and controls and operating within the agreed SLs:

• there have been no material administration errors in relation to processing core financial transactions; and

• all core financial transactions have been processed promptly and accurately.

The Trustee is also satisfied that there have been no material administration service issues during the year covered by this statement.

Member-borne charges and transaction costs

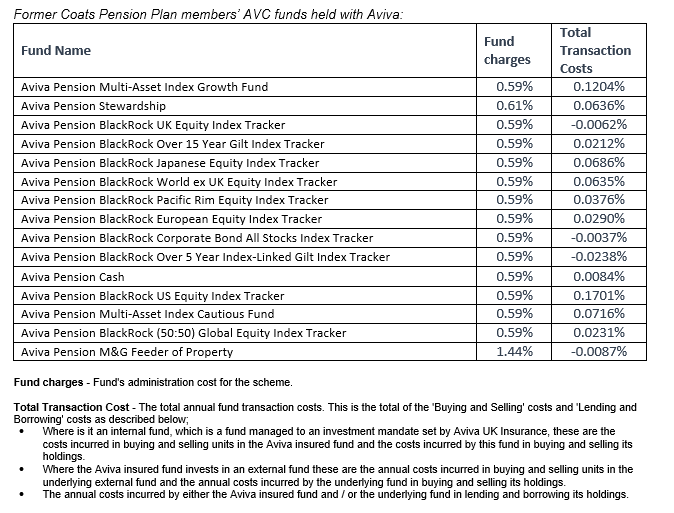

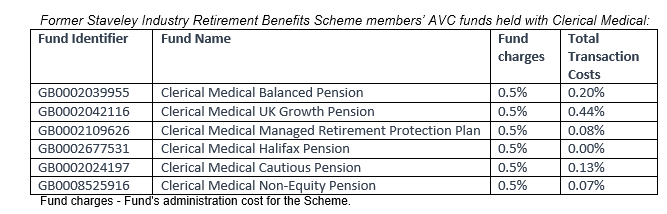

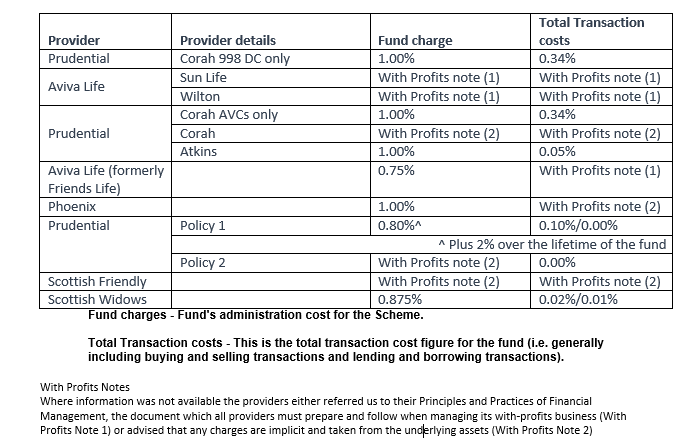

The Regulations require the Trustee to set out the charges and transaction costs incurred by members in this statement. The Trustee requested details of the charges and transaction costs from each of the providers of the 17 money purchase arrangements.

The information which has been obtained by the Trustee is detailed below, and represents a significant improvement on the information which had been provided last year with information provided on transaction costs by all the providers of unitised funds. The information provided by with profits funds is dealt with further on.

Former Brunel Holdings Pension Scheme members’ AVC funds held with Legal and General:

The only charge is the annual management charge (AMC) on the investment, this AMC of 0.75% is deducted from the unit prices before they are published.

Former Staveley Industry Retirement Benefits Scheme members’ AVC funds and Brunel Holdings Pension Scheme members’ AVC funds held with Equitable Life

During the period under review Equitable Life progressed a Proposal to close their with-profits fund and transfer all policies to Utmost Life and Pensions. The Trustee reviewed this proposal with the help of their Investment Adviser Redington, including the requirement to map the investment funds to the new funds available. The outcome was for the funds to move to unitised funds within Utmost and the 6 affected members were advised of the changes accordingly. As at the year-end the transition to the new funds was partially complete with the funds fully transitioned within 6 months of the date of the sale. The transaction costs and charges for the new funds are 0.75% plus transaction costs of <=0.3%.

The other 12 arrangements are conventional with-profits funds. Investors in with-profits funds do not get to see the actual value of the underlying assets. The value of the underlying fund changes daily, but customers’ fund values grow by a steady rate, called the regular bonus rate, which is calculated annually. Whilst the fund value grows steadily with regular bonus, it may be lower or higher than the value of the underlying assets. The charges are applied to the underlying assets, which adds complexity when providing details of the charges applicable to the members’ funds.

The results of our enquiries to the providers of these with-profits funds is below:

The Trustee continues to liaise with the providers, to be able to present more detailed information in future statements if possible. In particularas noted below the Trustee has engaged their investment adviser, Redington, to carry out a review of the DC funds on their behalf.

When preparing this section of the statement the Trustee has taken account of statutory guidance.

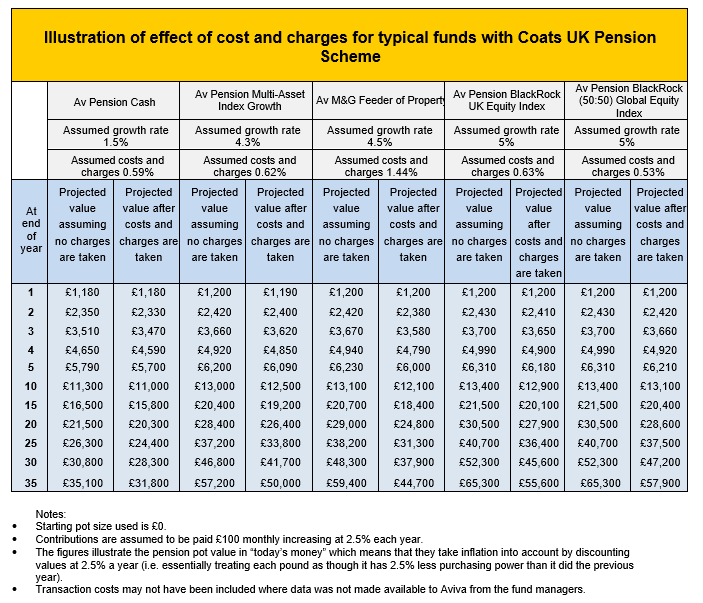

Illustration of charges and transaction costs

The legislation requires the Trustee to provide an illustrative example of the cumulative effect over time of the application of the charges and transaction costs noted in the previous section, on the value of a member’s accrued rights to money purchase benefits. The following table sets out an illustration of the impact of charges and transaction costs on the projection of an example member’s pension savings. The funds used in the illustration are funds available under the Aviva AVC arrangement. The majority of members’ money purchase benefits are held in the Aviva AVC arrangement.

To best illustrate the potential effect on members’ money purchase benefits of the charges being applied, the Aviva funds with the lowest and highest charges are included, together with funds with a range of investment returns. In determining the example illustration, the Trustee analysed the Scheme’s money purchase benefits, taking into account the range of member fund sizes, the range of investment returns and costs and charges across the various money purchase arrangements and the range of the expected periods of Scheme membership and the time it will take members to reach the Scheme’s normal pension age.

Under each fund there are two columns. The first shows the projected pension values assuming no charges are taken. The second shows the projected pension values after costs and charges are taken.

Value for members’ assessment

The Trustee is required to assess the extent to which the charges and transaction costs borne by members represent good value, taking into account the nature and needs of the members. In assessing value the Trustee has considered that value does not necessarily mean the lowest fee, and thus the quality of the other provisions was also considered.

In making the assessment and the statements below the Trustee considered any changes to operations as a result of COVID-19 as mentioned in the Trustee report section of the Annual Report and Financial Statements. Both Administrators, Coats Pensions Office and XPS put their business continuity plans into operation at the end of the Scheme year due to the lockdown arrangements in place at that time. The contingency plans ensured that priority was given to the paying of pensions, settlement of retirement benefits and the management of the Scheme’s financial requirements. They continue to have individuals working from home and have kept members up to date regarding COVID-19 via the website www.coatspensionsuk.com and with more detailed information for those members wishing to access their benefits.

All the Scheme’s other suppliers have in place arrangements to provide working from home facilities for their staff and have confirmed to the Trustee that this will not impact normal service. The Trustee continues to monitor the operational impact of the developments and has no significant concerns regarding the Scheme’s ongoing ability to fulfil its operational, cashflow or benefit payment requirements.

Whilst the Trustee did consider the calculation of transfer values as part of their review due to COVID-19 these were only put on hold for a short time, this did not affect DC transfer values and all such requests were dealt with in line with statutory requirements.

Charges and investment governance – for those schemes where full disclosure was obtained, the costs borne by members are reasonable when compared to general charges in the market including the charges cap on default funds. As noted above, the Trustee is continuing to pursue the providers to obtain the missing information in the meantime. Members have (where appropriate) access to a range of investment choices and can switch investment funds. Whilst no significant issues have been identified in the Trustee’s review of the performance of the unitised (non with-profits funds) the Trustee has commissioned a review of all the DC investment funds by their investment adviser Redington. Details of the findings including their review of the performance of the investment funds will be included in next year’s report.

Administration – The administrators are responsible for ensuring that the transactions processed by the third party providers of the money purchase benefits are accurate and timely and to report on any issues. The Trustee reviews the administration services, services levels and processes in place for the administrators which therefore include the provision of the DC benefits. The Trustee is happy that there are robust processes and procedures for logging and reporting issues with third party providers in place which ensure that the administration is carried out efficiently, and that all transactions were carried out in a timely manner with no issues to report.

Scheme management and governance – the Trustee is committed to the Scheme and ensures that the administration and operation of the money purchase benefits is monitored and regularly reviewed by the ARAC;

Communications – the administrators have a communications schedule and comprehensive procedures in place to review communications from a technical and member experience point of view to ensure that member communications are clear, tailored and communicative. Members receive timely and appropriate information about their money purchase benefits.

The majority of money purchase benefits are AVC’s additional to the accrued DB Scheme pension. AVC’s are typically used to fund tax-free cash in conjunction with the DB pension. For those members whose accrued benefits are pure money purchase in nature, the Trustee provides and pays for a third party service to enable annuity purchase. The member-borne charges for the Scheme’s money purchase benefits relate to the investment services and some communication services. All other charges in relation to the money purchase benefits and the Scheme are borne by the Sponsoring Employer.

Taking account of money purchase benefits under the Scheme and these services to our money purchase members relative to the costs incurred, the Trustee considers that, in general, the money purchase arrangements delivered good value for members for the year covered by this statement.

The Trustee’s assessment has been limited as value for members in respect of charges and transaction costs for with-profits funds cannot be easily assessed due to the structure of such funds and the incorporation of many costs in the annual bonus calculations. The Trustee has however acknowledged that due to the nature of with-profit funds it is not generally possible for the Trustee to improve the value of the funds.

The Trustee has taken account of the work by the previous Trustees for the three schemes which transferred their assets and liabilities to the Scheme in making this assessment. A review by a former scheme’s investment adviser was carried out, on 31 March 2017, into the DC funds under that Scheme. This included the Aviva AVC funds and the majority of the with-profits funds. That review concluded that the with-profits funds should not be reorganised, given the likely value implicit within the guaranteed rates of annuities that they provide.

The Trustee has now commissioned a full review of the DC funds, following the review completed by the previous Scheme in 2017 and will report further in the next statement.

The Trustee also notes the work carried out on the Financial Conduct Authority on the fair treatment of with-profits customers and will continue to monitor the responses from the with-profits providers in conjunction with the findings of that review.

Trustee’s knowledge and understanding

The law requires the Trustee Board to possess, or have access to, sufficient knowledge and understanding to run the Scheme effectively.

The two professional independent Trustee firms on the Trustee Board, Independent Trustee Services Limited, and Capital Cranfield Pension Trustees Limited, each have experience of sitting on major DC schemes. Their representatives have used their experience since appointment in 2018 to ensure that they understand the details of the Scheme and therefore bring to the Scheme extensive understanding and experience of DC governance and best practice.

The Trustee Directors take our training and development responsibilities seriously and keep a record of the training completed by each member of the Board. The Trustee uses these logs to keep track of our reviews of Scheme documents and policies to ensure that each Trustee Director has a good working knowledge of Scheme documents. The Trustee ensures that training requirements are reviewed annually, with the last review taking place in November 2019, to identify any gaps in the knowledge and understanding across the Board as a whole, and the Trustee continues to work with its professional advisers to fill in any gaps, either individual or collective.

Specific actions include:

• An induction process is in place for new Trustee Directors covering the law relating to pensions and trusts, and the relevant principles relating to the funding and investment of occupational pension schemes. This includes completing the Pension Regulators Trustee Knowledge and Understanding toolkit and training with the Scheme’s actuarial and investment advisors. Over the year under review, on 27 September 2019, Claire Thompson was appointed as a Trustee Director.

• An annual training day is held to ensure the Trustee Board is up to date on current pension issues, emerging regulation and governance best practice including DC. This year the training was held on 13 November 2019.

• Throughout the year, the Trustee Directors have access to various training and seminar events.

• Where appropriate, the Trustee’s professional advisers attend Trustee Board and sub-committee meetings supporting the Trustee in ensuring that it exercises its functions properly and advising on applicable laws, and funding and investment principles, as appropriate.

• Reference is made at Trustee Board and sub-committee meetings to relevant sections of the Scheme’s trust deed and rules, Statement of Investment Principles and Trustee policy documents (including CUKPS DC benefits principles) to maintain Trustee Directors’ understanding of these documents.

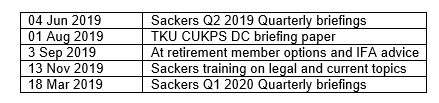

The Trustee’s training logs detail the quarterly updates from their legal advisers who provide quarterly updates on DC pension topics which are relevant to the Trustee Board, along with any additional training completed over the year. This year the logs included the following training including DC topics:

As a result of the training activities which have been completed by the Trustee Directors individually and collectively as a Board, and taking into account the professional advice available to the Trustee, I am confident that the combined knowledge and understanding of the Board enables us to exercise properly our function as the Trustee of the Scheme.

The statement regarding DC governance was approved by the Trustee and signed on its behalf by:

Mr C Martin

Independent Trustee Services Limited

September 2020